- The Hot Startups

- Posts

- 5 Government Schemes Every Indian Startup Founder Should Know

5 Government Schemes Every Indian Startup Founder Should Know

Grants, tax holidays, and debt programs that actually help startups scale

Dhara Mandaliya

January 16, 2026 • Reading Time: 3 minutes

Happy National Startup Day!

In India, the startup ecosystem has undergone a massive boost in the last 2 decades, especially with the 2016 initiative by the Government of India - Startup India.

Fund of Funds for Startups solved the scaling problem of startups with a ₹10,000 crore initiative. DPIIT has recognised 2.09 lakh startups, which have also generated 21 lakh jobs in the past decade. (Source)

Let’s look at five government schemes that you can look into to take your startup to the next level.

Some of our recent stories:

Can you challenge Colgate?

(Perfora says YES)K L Rahul and Katrin Kaif’s bet on wellness

(HyugaLife’s startup journey of building consumer trust)On Getting Selected by Gully Boy

(Urban Monkey’s No VC Startup Journey)

1. Startup India Seed Fund Scheme (SISFS)

What It Offers: Up to ₹20 lakh as a grant for proof of concept, prototype development, or product trials. An additional ₹50 lakh available for commercialization and scaling. (Source)

Why It Matters: This addresses the hardest funding gap - the pre-revenue stage where angels fear to invest and bootstrapping hits limits. The grant portion requires no equity dilution or repayment. The fund operates through 300+ recognized incubators who provide mentorship alongside capital.

The Structure: Disbursement happens in milestones, not lump sums. You define clear deliverables - completing a prototype, testing the product, achieving technical validation - and receive tranches as you hit targets.

Total Corpus: ₹945 crores, ₹227 crores from which has been deployed to 1,200+ women-led schemes.

Best For: DeepTech, hardware, biotech, and any capital-intensive sector where building a working prototype requires significant upfront investment before you can demonstrate traction.

2. Fund of Funds for Startups (FFS)

What It Offers: A ₹10,000 crore corpus that supports 88 Alternative Investment Funds (AIFs), which then deploy capital to startups across stages.

This isn't direct funding - it's a multiplier mechanism. Government capital flowing into AIFs makes those funds more credible to institutional investors, catalyzing additional private capital. An AIF backed by FFS finds it easier to close its target corpus and can take bigger bets on emerging sectors.

The Ripple Effect: The structure acknowledges that government bureaucrats shouldn't pick startups, but government capital can de-risk an otherwise conservative private ecosystem.

Who Benefits: Mid to late-stage startups. This scheme works indirectly - you don't apply to FFS; you raise from AIFs that FFS has backed.

Also Read: India’s Government-Led Agri-Tech Boom

3. DPIIT Recognition Tax Benefits

What It Offers: 100% tax holiday for any three consecutive years within your first ten years of operation. An 80% rebate on patent filing fees. Self-certification for 6 labor laws and 3 environmental laws.

The Compliance Advantage: Self-certification reduces the bureaucratic burden during fragile early years. Instead of navigating inspections and audits for labor and environmental compliance, you certify adherence yourself. This saves time and legal costs when every hour matters.

The Impact: 50% of DPIIT-recognized startups now operate in tier-two and tier-three cities, a good indicator of democratization of startup funding.

Eligibility: DPIIT recognition requires incorporation as a private limited company, partnership, or LLP; turnover under ₹100 crore; entity age under 10 years; and working toward innovation or scalability.

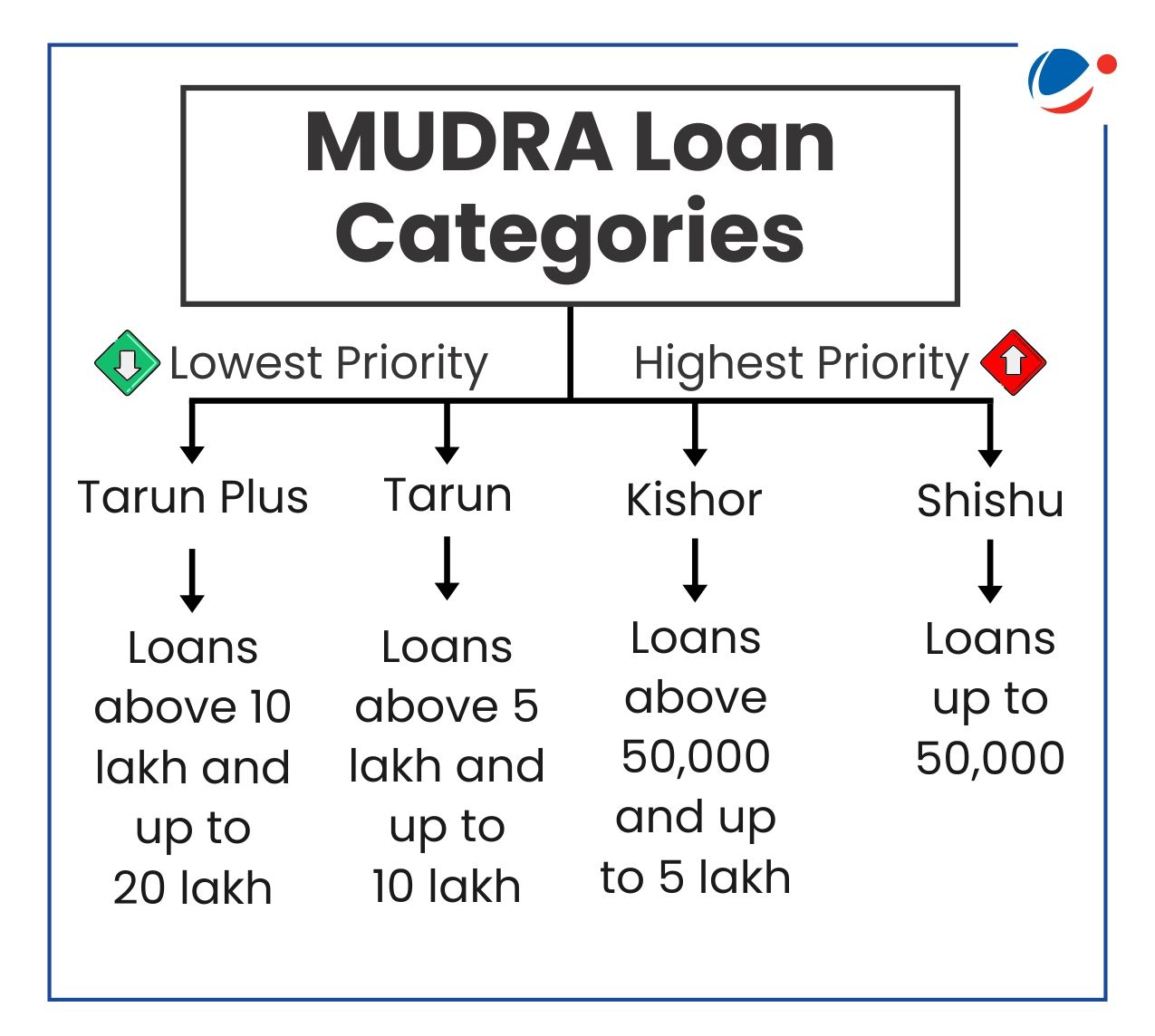

4. Pradhan Mantri Mudra Yojana (PMMY)

What It Offers: Collateral-free loans up to ₹20 lakh across these tiers:

Why It Matters: This funds the un-fundable - micro-enterprises that will never raise venture capital but create the bulk of India's employment. By 2025, PMMY has disbursed ₹32.61 lakh crore, making it the largest microfinance program in India.

The Reality Check: Interest rates vary by bank and borrower profile, typically ranging from 8-12%. Repayment tenure extends up to seven years. The real benefit is access without collateral for entrepreneurs who lack property to mortgage.

Best For: Service businesses, retail, small manufacturing, and any venture requiring ₹20 lakh or less with a clear path to cash flow.

5. Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE)

What It Offers: Guarantees up to 85% of loans extended to micro and small enterprises, covering amounts up to ₹5 crore. (Source)

Why It Matters: Banks are risk-averse, especially with startups lacking collateral. CGTMSE changes the math. When 85% of a loan is guaranteed, banks approve applications they'd otherwise reject. This transforms access to debt capital without requiring you to mortgage personal assets.

The Mechanics: You don't apply to CGTMSE directly. You apply for a loan at a participating bank, which then seeks CGTMSE coverage. The guarantee fee is nominal - typically 0.37-1.2% annually - and gets factored into your loan terms.

The Enhancement: For DPIIT-recognized startups, the guarantee ceiling jumps to ₹20 crore, opening up growth-stage debt financing that was previously inaccessible without substantial collateral.

The Broader Shift

India's startup narrative has centered venture capital for too long. But many are building businesses with personal savings, family money, bank loans, and increasingly, government schemes.

Government schemes democratize entrepreneurship beyond the IIT-IIM-VC circuit. They fund the un-fundable, de-risk the risky, and make business creation accessible.

If used correctly, it can be a powerful supplement that extends runway, reduces dilution, and provides breathing room to reach profitability or the next private funding milestone.

Reply